Here’s a pattern I’ve seen over and over:

Loan officers obsess over the objections they get or even haven’t actually gotten, but afraid they will…

But the real danger is the objections they never hear, because they never asked for the business in the first place.

If you don’t ask a borrower to work with you, or a realtor to send you a buyer…

You’re not avoiding rejection.

You’re avoiding revenue.

So LOs talk, present, quote, nurture, compare, calculate…

…and hang up without ever saying the only sentence that matters:

“Based on what we discussed, I’d love to take care of this for you. Should we get started?”

And here’s the wild twist:

When you don’t ask, the borrower creates their own objection stack in silence:

- “Maybe I should shop this.”

- “Maybe there’s someone cheaper.”

- “Maybe I’m bothering her / him.”

- “Maybe he’s / she’s busy.”

You never get to rebut those.

Because you never earned them; you never asked.

Top producers don’t close more because they get fewer objections (they actually get MORE objections).

They close more because they trigger the right ones early by asking for business, handling them by using success scripts, and moving forward with permission.

Saturday Strategy:

- Ask for the business. Always.

- Use a script to do it so your tone stays calm, certain, and human.

- When you hit voicemail, leave a curiosity-based script that sets up the next conversation, not a novel, not a pitch.

- Send the follow-up text that refers back to the script and asks again in one clean line.

Because:

The objection that matters most is the one you never asked for.

Want my 3-part script pack for:

- Asking for business without sounding weird

- Voicemail strategy that creates replies

- Follow-up text that re-opens the deal

We’ll go over that and more on a 30 min 1 on 1 zoom call here

We’ll show you exactly what to say and how to say it whether you join us or not, because that’s how we roll around here.

We help others how we want to be helped 🙂

It’s your turn now, let’s set up a private chat here.

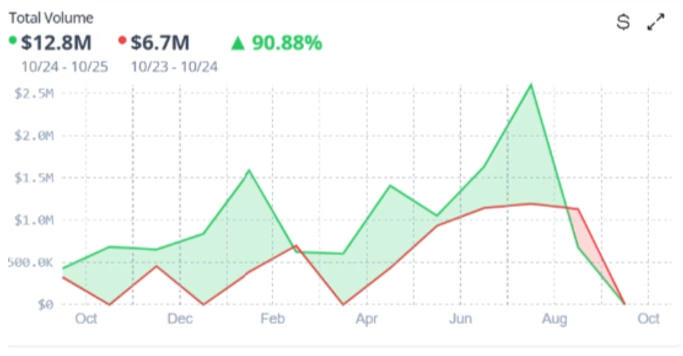

Red line = last year

Red line = last year Green line = this year

Green line = this year